As global equity markets continue to grapple with a host of geopolitical and economic concerns, such as the war in Ukraine, elevated inflation, and fears about a potential recession, your clients may have a lot of questions.

The Portfolio Managers of the JOHCM Emerging Markets Opportunities Fund (JOEMX) continue to stress to clients and prospective investors the following key elements.

Summary

- The JOHCM Emerging Markets Opportunities Fund was founded on the basis that “Investing in Emerging Markets equities goes right or wrong at the country level.”

- Investors should be looking to capitalize on the new leaders in emerging markets, which we believe are countries and sectors that stand to benefit from the economic shifts emanating from global matters.

- Some (not all) Emerging Markets are attractively positioned for growth. We feel that investors may be overlooking these strengths.

Leveraging Top-Down Opportunities in Emerging Markets

Emerging Markets offer a far more diverse country universe (24 countries) than developed markets, encompassing a much wider variety of economic development, political systems, natural resource endowment, industrial composition, and openness. Overlaying that diversity is a history of booms and busts that have occurred predominantly at the country level. Each country has its own economic model for development that may experience divergent levels of success depending on the global economic cycle. This exposes Emerging Markets to more macro- economic vulnerabilities, particularly in short, sharp bursts.

The JOHCM Emerging Markets Opportunities Fund (JOEMX) was founded on the basis that “Investing in Emerging Markets equities goes right or wrong at the country level.”

The JOEMX team has over 30 years of experience investing in Emerging Markets. During this period, they have encountered the powerful investment opportunities that top-down can offer in an asset class characterized by national boom and bust cycles. This, along with the team’s own research, has driven their philosophy that country selection is the single most important component of Emerging Markets investing.

EM stocks exhibit a notable correlation with the country they’re domiciled in, implying that macroeconomic factors such as interest rates, currency fluctuations, political risk, and overall economic growth drive these equities from the top-down. The team takes high-conviction country positions to exploit top-down, country-level opportunities that they believe are overlooked by the bottom-up investors who dominate the asset class.

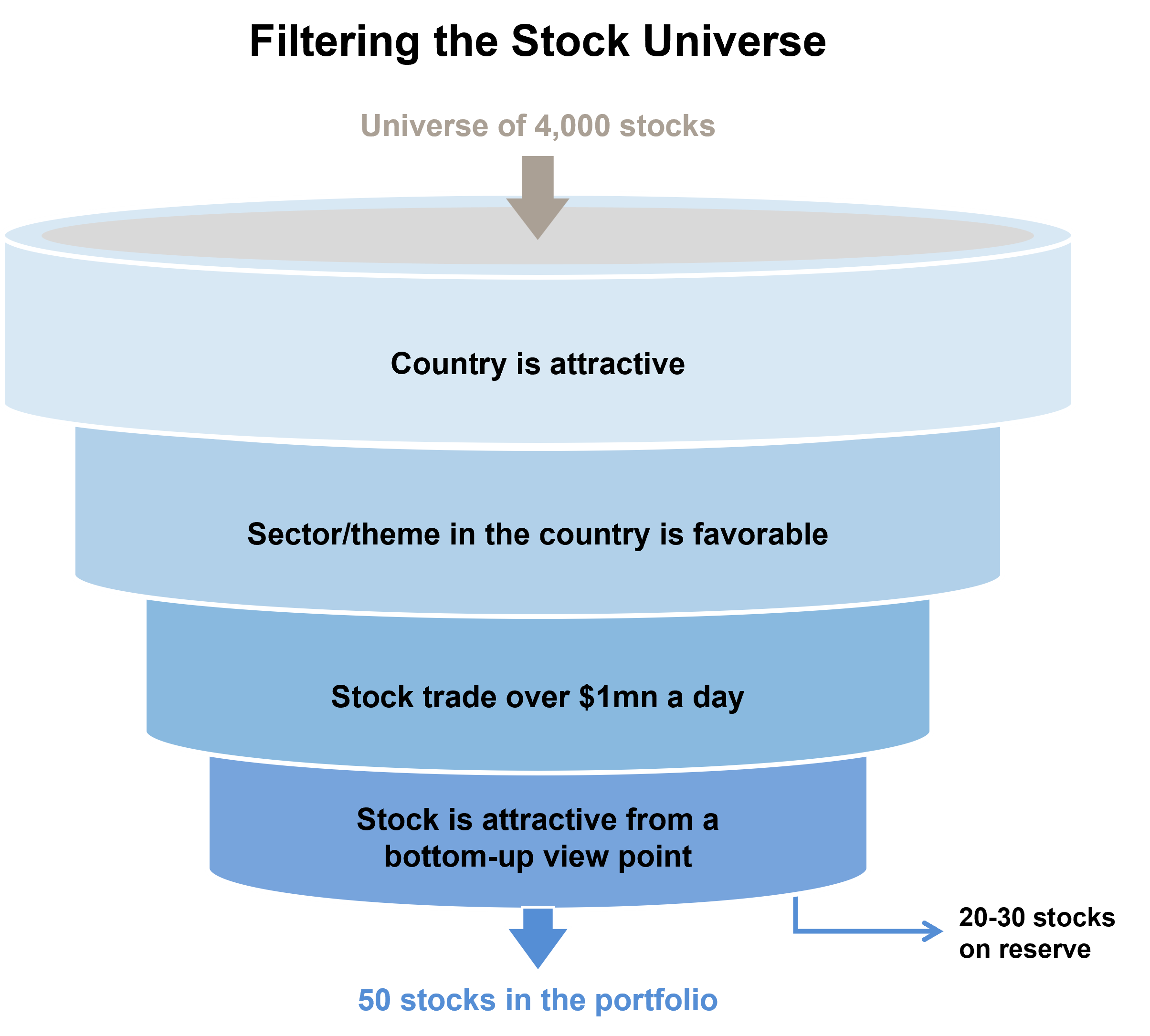

Typically, the Fund is invested in only half the markets in the benchmark with preferred sectors and themes in each of those countries. Therefore, the team not only focuses on country selection as a source of alpha, but also seeks to own stocks in the parts of the economy and equity market that should benefit most from the top-down environment foreseen.

Overall, JOEMX’s approach creates a portfolio with a high active share compared to the index, and an all-cap approach with a focus on liquidity. While the team acknowledges the importance of bottom-up analysis, they believe that macroeconomic inputs into bottom-up models are more important in Emerging Markets than they are in the developed world.

We Are in the Midst of a Regime Shift

The last few years in Emerging Markets has been dominated by growth, momentum, and, to a large extent, speculative Chinese technology. However, it is increasingly evident that a new set of leaders may be emerging. We believe these new leaders will benefit from the economic shifts emanating from the Ukraine conflict, as well as multi-decade high inflation, the direction of the US Dollar, and geopolitical uncertainty. We see potential opportunities in:

- Resource-rich countries heavy on exports, such as Brazil, South Africa, and Mexico

- Cyclical economies well positioned for economic growth powered by increased lending from high-quality banks – like Indian banks

- Countries whose central banks have already taken measures to rein in inflation, such as Brazil

Successfully navigating the challenges and opportunities ahead will require differentiated exposure with an eye for country selection. Is your portfolio prepared?

Why are we excited about the setup for Emerging Market Equities Now and How JOEMX Fits?

While no two market regimes are exactly the same, we can draw parallels from the past. The current environment for EM Equities appears similar to the last period of pronounced EM equity market outperformance from 2002 to 2007—indicating that it could be an opportune time to invest in this asset class.1

From that cycle we learned that higher commodity prices tend to positively impact emerging markets and that higher interest rates aren’t necessarily an impediment. From 2002 to 2007 the Fed hiked rates seventeen times, from 1% to 5.25%, and this didn’t prevent the asset class’s standout performance. One of the main differences between the 2002 to 2007 cycle and the current environment is the relative weakness of China today compared to several years ago. We believe JOEMX’s country-driven approach is well positioned to navigate the volatility resulting from heightened geopolitical uncertainty.

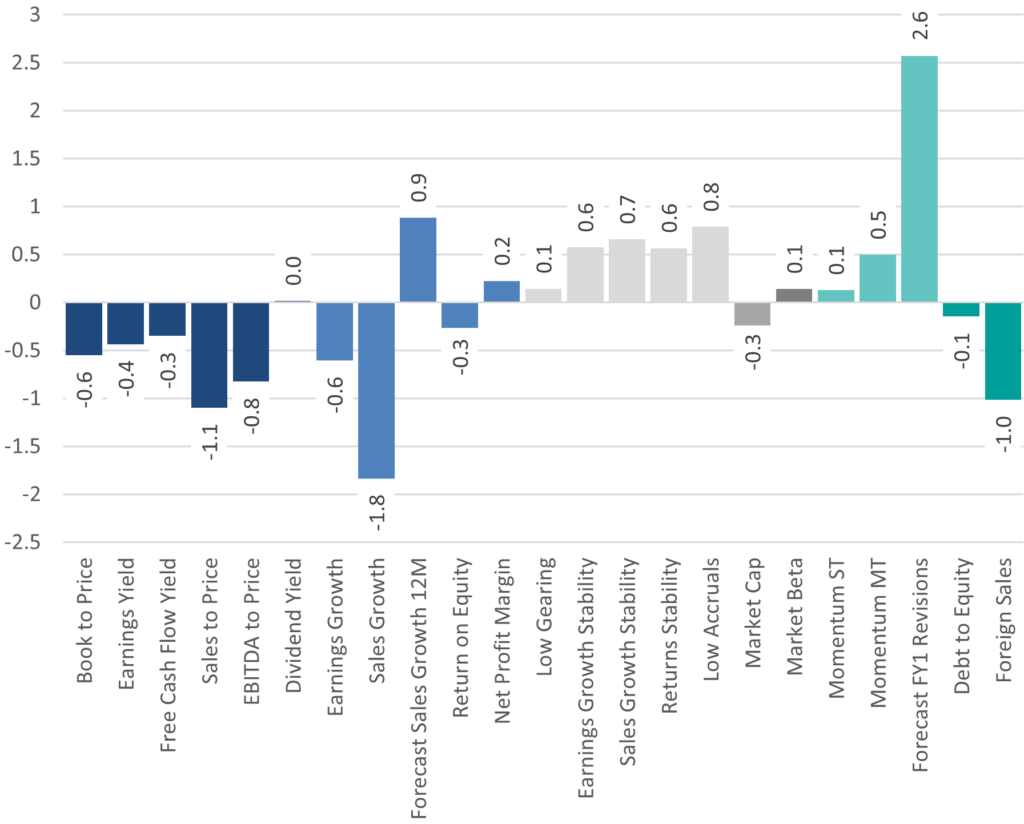

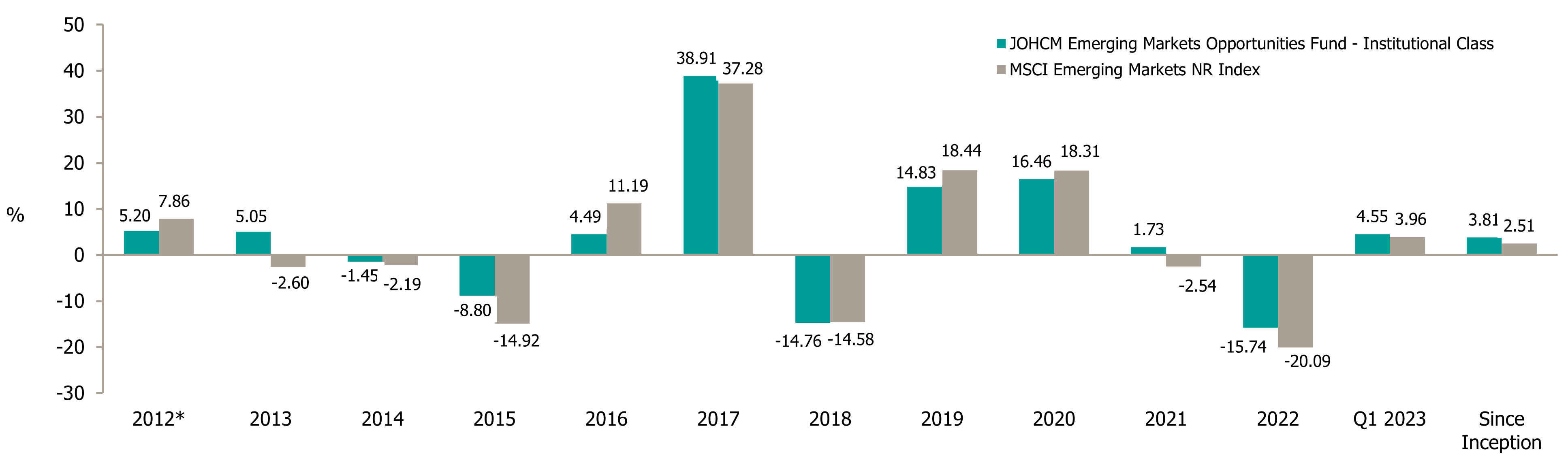

The Portfolio Managers of the Fund believe that valuation discipline is important in Emerging Markets and would describe their approach as Growth at a Reasonable Price (GARP), by seeking to invest in companies with attractive fundamentals at a reasonable price. This valuation discipline often leads to resiliency in volatile periods. The fund has historically outperformed in most down markets (2013, 2015, 2021, and 2022), which provides a distinct counterbalance to aggressive growth/momentum-oriented EM strategies.

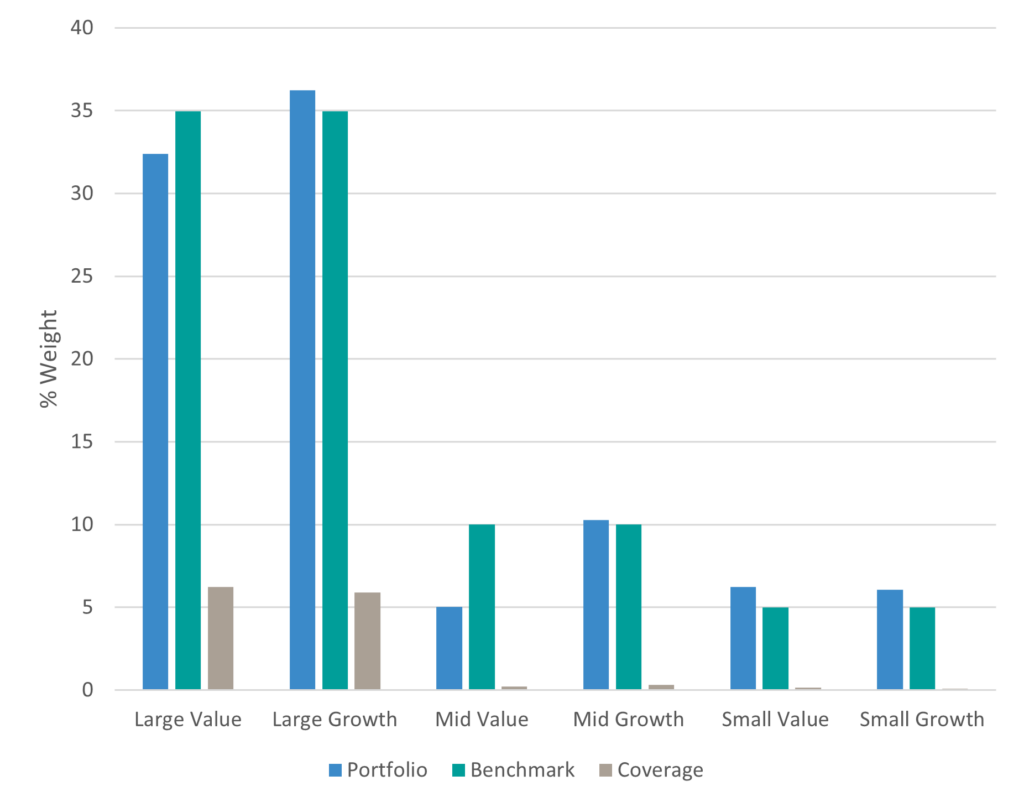

The team monitors the portfolio’s style positioning to ensure that there is no excessive exposure to style biases, such as value or growth stocks or high or low momentum stocks. Below, you can see JOEMX’s unique style/factor distribution and how it differentiates itself from the index.

Portfolio Style Skyline™

Style Distribution

Capturing opportunities in Emerging Markets

From the period spanning 2006 – 2021, the average annual performance of the worst performing EM country was -32%, while the average annual performance of the top performing EM country was 54%.2 In other words, the difference between the best- and worst-performing countries was more than 80% percent each year, on average.

The JOEMX Portfolio Management Team aims to concentrate the portfolio in Emerging Markets where the team sees favorable conditions for equities and the greatest opportunity to construct a genuinely diversified and different portfolio than peers.

Emerging market equity is a broad and diverse asset class, and there will always be countries and markets doing better than others. Despite concerns about inflation, monetary policy, and geopolitical uncertainty, the current macroeconomic landscape is highly supportive for some (but not all) emerging markets. We feel investors may overlook these strengths and continue to seek opportunities where we see the best top-down conditions.

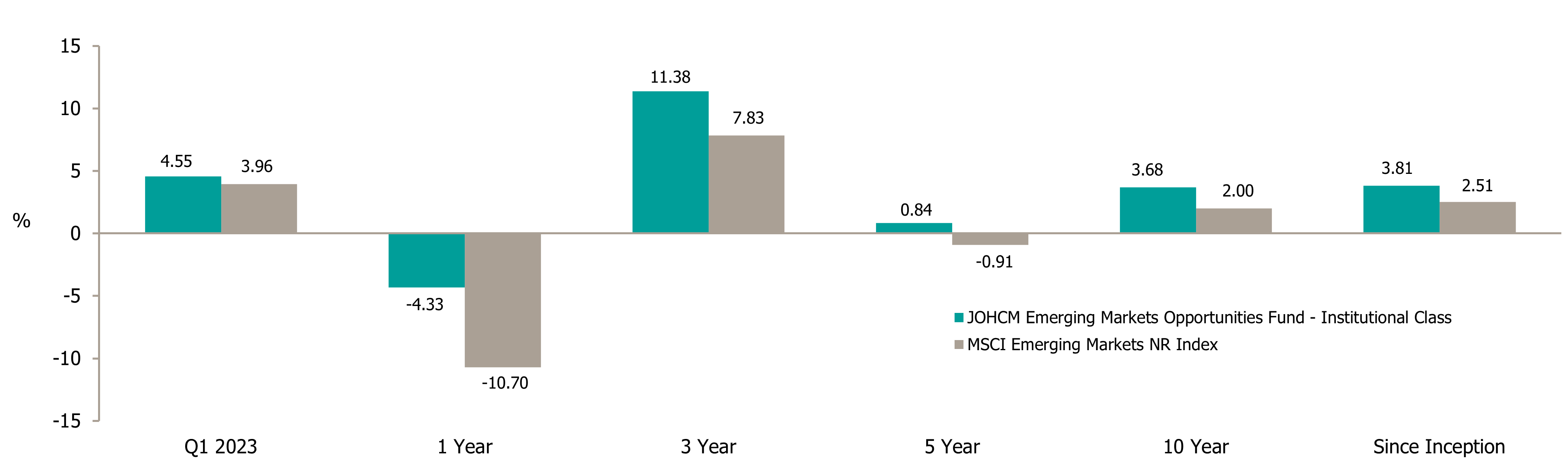

Performance – Total Returns (USD) as of March 31, 2023

The performance data quoted represent past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance data quoted. Investors may obtain performance information current to the most recent month-end, within 7 business days at www.johcm.com or by calling 866-260-9549 or 312-557-5913.